Mary Beth Eastman

Mary Beth Eastman

Key Takeaways

- Overall, the housing market is expected to remain challenging, especially for younger buyers and those without substantial equity.

- Mortgage experts predict continued rate volatility, with many seeing 30-year fixed interest rates landing close to 6% by the end of the year.

- Home prices, which skyrocketed since 2022, will still trend upward, but the increase should be much gentler this year.

- Savvy buyers and homeowners will get their financial ducks in a row early to be ready to buy, sell or refinance when rates and prices reach a favorable equilibrium.

While 2024 didn’t deliver the lower mortgage rates and home prices that many had hoped for, the U.S.’s surprisingly resilient economy did deliver one of the most buyer-friendly markets since 2016, according to a report from the National Association of Realtors. That’s saying something, since the year concluded with 30-year fixed purchase mortgage interest rates averaging 6.85%, according to Freddie Mac data.

Higher home prices and interest rates meant more homes lingered for sale in 2024, slightly increasing supply while softening demand and creating a bit of breathing room. However, it’s still a seller’s market with fewer than four months of inventory, and affordability remains a stubborn stumbling block for many.

“From an affordability perspective, we think 2025 will look a lot like 2024, with mortgage rates above 6 percent, home price growth easing from recent highs but staying positive, and supply remaining below pre-pandemic levels,” said Mark Palim, Fannie Mae senior vice president and chief economist, in a December statement.

For 2025, many industry experts are forecasting mortgage interest rates to hold steady in the mid-6% range, while home appreciation should range between 1% and 4%. This could possibly open new opportunities to buy, sell, or tap your equity when the timing is right. In this article, we’ll review the top predictions for the year ahead and share tips for optimizing your housing moves in 2025.

Mortgage Rates Will Probably Stay Above 6%

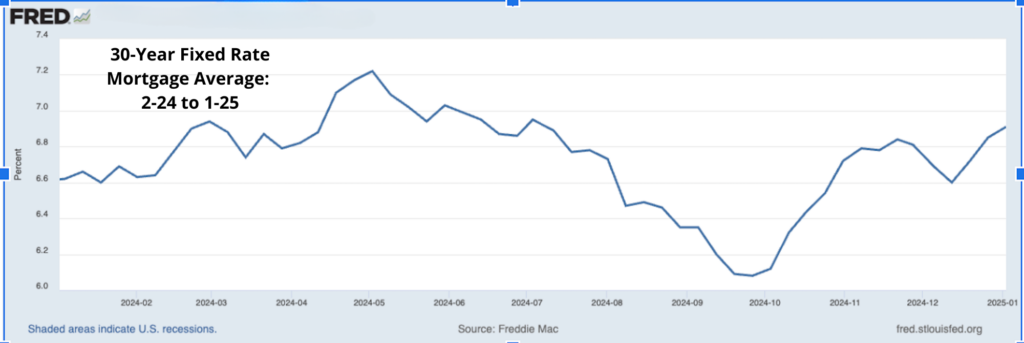

Although there was a brief window of time in late September 2024 when average mortgage interest rates brushed the 6% mark, it was short-lived. The rate roller-coaster climbed back above 6.8% by year’s-end, as shown in the Federal Reserve chart below – lower than the year’s spring peak of 7.22% in May, but not by much.

Source: Federal Reserve Bank of St. Louis

“Our advice is to plan and budget for the mid-6% range” for 2025, said the economists behind Realtor.com’s 2025 housing market forecast, predicting a monthly average rate of 6.3%. Fannie Mae’s economists echo a similar outlook, stating they expect mortgage rates to “decline modestly” but stay above 6%, with “likely bouts of volatility” throughout the year.

The National Association of Home Builders had a slightly more optimistic take in November, expecting mortgage interest rates to fall below 6% by the end of 2025. However, with December’s cut to the fed funds rate already priced in, upward revisions may be the name of the game, at least for the 30-year fixed mortgage; Wells Fargo revised its forecast for 2025 up a third of a percentage point in December, while the Mortgage Bankers Association now expects rates to sit between 6.4% and 6.6%.

- Refinance rates: Expect elevated rates for mortgage refinancing in 2025 too, though an overall lower interest rate environment could make refinancing more attractive for homeowners who bought during higher-rate periods.

- Home equity loan / HELOC rates: Expect these to trend lower but remain in the 7% range, predicts Bankrate, which is forecasting HELOCs to average 7.25% and home equity loans to average 7.90 percent in 2025.

Home Sales Will Grow 1.5%

Existing home sales were “subdued” in 2024, according to a Freddie Mac analysis. With rates staying relatively stable, expect a continuation of that trend in 2025, with modest sales growth and appreciation in the new year. Fannie Mae’s forecast suggests national home price growth will decelerate, perhaps providing some relief for buyers but slowing down appreciation for owners. If a new home is on your 2025 bingo card, you can expect a “friendlier, less competitive housing market,” according to Realtor.com’s forecast.

Pricing

Home prices will grow by 3.7%, per Realtor.com. Zillow’s forecast is slightly more modest, predicting a 2.6% average increase in home value for 2025. The Mortgage Bankers Association sees a median existing-home price of $405,200 by year’s end, with new homes at a median price of $418,400.

Inventory

According to Redfin data, housing supply is up 12% year-over-year, with many buyers hanging back because of high prices. Realtor.com’s forecast expects existing for-sale inventory to be almost 12% higher in 2025.

Sales trends

Predicting that new home sales will be a “bright spot” in the housing market, Fannie Mae’s forecast also cautions that location will play a key role. Meanwhile, Realtor.com’s forecast calls for a 1.5% rise year-over-year in home sales, to 4.07 million, while MBA’s mortgage finance forecast expects 3.1 million new homes, per its December report.

7 Strategic Moves for Homeowners

No matter what your housing goals are for 2025, there are some steps you should take to position yourself for maximum success, whether you’re buying, selling, or staying put.

- Lock in on your goals: Know what you want to do and plan how to achieve your goals. With rates staying steady but home prices slated to rise, waiting isn’t always the move.

- Bolster your finances: Prepare yourself financially by building savings and improving your credit score, especially if you are renting or a first-time homebuyer. Not only will you be better prepared for opportunities as they arise, but you’ll be more likely to qualify for a lower interest rate with a stronger financial profile.

- Build a bench of pros: Now’s the best time to secure your team, including experienced and qualified real estate agents, mortgage brokers, loan officers and even home insurance pros. These experts can help you make smart decisions, and the best ones have a proactive approach to the housing market’s many nuances.

- Know your local market: It bears repeating that real estate is a local concern. Nationwide trends are important to be aware of, but your local market matters much more when it comes to supply, pricing, and appreciation.

- Be prepared to act fast: Mortgage rates change by the hour. With more volatility on the horizon, being ready to jump on an opportunity can give you a competitive advantage in real estate transactions and home loans.

- Shop around: When shopping for a mortgage loan, refinance, home equity loan, or other form of financing, comparing lenders and offers is a must. Keep in mind that the lowest rate isn’t always the best deal; make sure to compare fees, service, and quality, too.

- Know your equity: Moving isn’t your only option. If you’ve gained appreciable equity in your current home, you might want to tap it for cash instead. Do some market research and enlist a real estate agent or appraiser to give you a current market value, which you can compare to your outstanding mortgage balance. A home equity loan or line of credit could provide access to your equity, but both carry interest charges. For a way to tap equity without borrowing, consider a home equity agreement, which offers homeowners a lump sum payment in exchange for a portion of your home’s future value. Unlock’s home equity agreements have no monthly payments or interest charges while still providing cash for expenses or home improvements.

While any number of surprises could be in store for homeowners and buyers in 2025, being prepared is key. Keep an eye on market trends as the year progresses and you’ll be prepared to reach your goals when the timing is right.